July 2014 – An Economic and Market Update

EXECUTIVE SUMMARY

- The Dow Jones Index set a new record in what has been a positive year for most asset classes.

- Unemployment in the United States is improving, but there is cause for concern as the long-term unemployment rate remains elevated.

- The Fed continues to exert control over inflation and interest rates, despite being in uncharted territory due to the various iterations of Quantitative Easing.

- The downward revision to GDP in the First Quarter of 2014 disappointed Wall Street, but was overshadowed by improvements in other areas of the economy that point to continued economic growth.

LOOKING BACK

| MAJOR STOCK INDICES | YTD 2014 |

| S&P 500 | +6.24% |

| Russell 2000 | +3.06% |

| DJ UBS Comdty | +7.36% |

| Barclays Bond Agg | +2.59% |

| MSCI EAFA | +1.29% |

| Wilshire US REIT | +14.76% |

January 1, 2014 to June 30, 2014

| |

The Second Quarter came to an end with the Dow Jones Industrial Average at 16,826.6. In the first few days of July the DJIA briefly entered 17,000+ territory for the first time in history. Not to be overshadowed by the stock market, the Unites States energy industry was officially named the world’s largest producer of oil and natural gas liquids by the International Energy Agency, and the U.S. economy added 288,000 jobs in the Second Quarter.[i][ii]

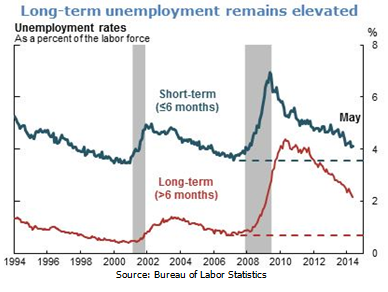

UNEMPLOYMENT IN A NUTSHELL

The unemployment rate in the Unites States continued its downward trend as reported by the Bureau of Labor Statistics for June. The Civilian Unemployment Rate, which quantifies those individuals seeking jobs over the total size of the labor force, is now equal to the 50-year average and represents a marked improvement over the high experienced in October of 2009. While the increased number of jobs is encouraging, it is clear there is a growing disparity between the short-term unemployed, those out of work for less than 6 months, and the long-term unemployed, those continuously unemployed for 6 months or longer.[iii]

Short-term unemployment has reached a relatively normal and healthy state nearing pre-recession levels. The long-term rate, however, remains elevated at a rate more than double the historic average. There is potential for the long-term unemployment to become a drag on economic growth if this trend continues.[iv]

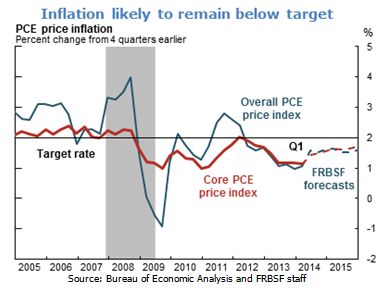

THE FED: INFLATION AND INTEREST RATES

We are watching closely as the Federal Reserve transitions away from its bond buying policy under Quantitative Easing later this year. The two primary areas of focus are the Federal Reserve’s ability to target and manage a healthy rate of inflation and the setting of interest rates. For now, interest rates continue to be historically low and economic data is showing signs that inflation rates are moving upward towards the Federal Reserve’s target of 2%.[v]

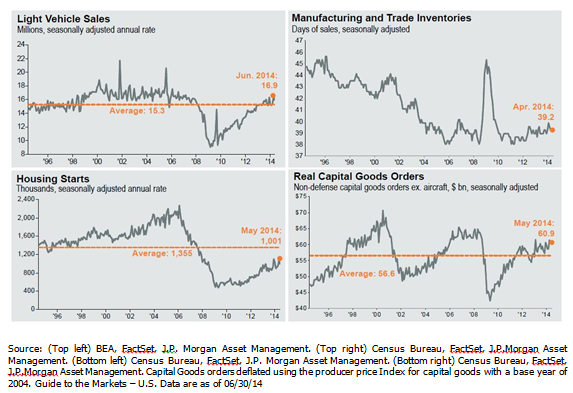

GDP: THE ENGINE THAT COULD

In the First Quarter of 2014 bad weather negatively impacted our domestic economy, with Gross Domestic Product (GDP) decreasing at an annualized rate of 2.9%. According to the Bureau of Economic Analysis, “The decrease in real GDP in the first quarter primarily reflected negative contributions from private inventory investment, exports, state and local government spending, nonresidential fixed investment, and residential fixed investment.”[vi]

Despite the weather, the above data show that across many of the significant contributors to GDP, improvement to the long term average has/is occurring. Forward looking GDP projections are positive and the recent job creation number of 288,000 private sector jobs has many economists beginning to be positive on the direction of the economy.

LOOKING FORWARD

We look forward to the Federal Open Market Committee meeting on September 16/17 for continued direction from the Federal Reserve and Fed Chairwoman Janet Yellen. In addition to the Third Quarter FOMC meeting, the Bureau of Economic Analysis will be releasing the advance estimate of Second Quarter GDP growth on July 30th. The current consensus is that this will show a strengthening economy recovered from the difficult weather concerns of the First Quarter.

Significant foreign conflicts (as in the Middle East, Russia/Ukraine, North Korea, China/Taiwan/South China Sea, and so on) may also impact our domestic economy going forward and we follow global events carefully.

We remain committed to the protection of your assets and the growth of your investment portfolio. We are focused on protecting value, providing you with trusted advice, and assisting you and your family in making good decisions.

Thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Diversification nor asset allocation assure a profit or protect against a loss in declining markets.

Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean Storck and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Rawdin-Baron Financial, Inc. IMS platform accounts offered through 1st Global Advisors, Inc. Rawdin-Baron Financial, Inc. and 1st Global Capital Corp. are unaffiliated entities. Rawdin-Baron Financial, Inc. is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean Storck #0F25995 and Nicole Albrecht #0F99962.

Copyright © 2014 Rawdin-Baron Financial Inc., all rights reserved.

Rawdin-Baron Financial, Inc., 4747 Morena Blvd, Ste 102, San Diego, CA 92117

[i] Bloomberg.com, “US Seen as Biggest Oil Producer After Overtaking Saudi Arabia”, 07/04/14

[ii] Bureau of Labor Statistics

[iii] Bureau of Labor Statistics

[iv] Rob Valletta, Federal Reserve Bank of San Francisco, FedViews, Twelfth Federal Reserve Disctrict, June 12, 2014

[v] Rob Valletta, Federal Reserve Bank of San Francisco, FedViews, Twelfth Federal Reserve Disctrict, June 12, 2014

[vi] Bureau of Economic Analysis, Gross Domestic Product: First Quarter 2014 (Third Estimate)