April 2017 – An Economic and Market Update

AN ECONOMIC AND MARKET UPDATE

Quarterly Market Update – April 2017

![]()

- Politics has dominated the headlines so far in 2017. The 1st Quarter was focused on the incoming Trump Administration. The 2nd Quarter will serve as witness to the French Election and the potential consequences if a Euro-sceptic is voted in.

- In dog years the current bull market is getting quite old. Market metrics point towards reduced returns in the near to mid-term relative to the growth of the last 8 years.

- When stocks show signs of getting expensive rational investing behavior is more important than ever. It is not a time to look for the next “thing” so much as reinforcing investing strategies such as rebalancing and diversification.

LOOKING BACK

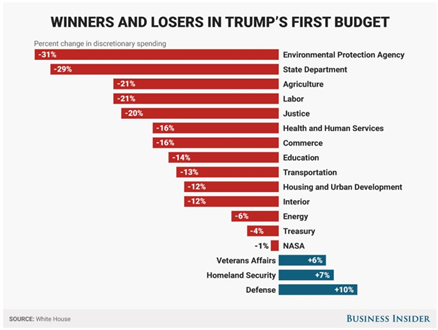

The 1st Quarter of 2017 felt like an echo chamber the way all eyes and ears were trained on the decisions of the incoming Trump Administration. The over-saturation of media coverage makes it feel like he has been in office for much longer than 3 months. The economic success or failure of President Trump will not be known for quite some time. What we know right now through a flurry of executive actions: we are out of the Trans Pacific Partnership, the Federal Government is on a hiring freeze, our new President is a big fan of deregulation across the board, and there are some very clear winners and losers in his first proposed budget.

Source: Business Insider as compiled from White House releases

In order to increase defense spending President Trump has recommended, “that Congress enact non-defense discretionary reductions of $18 billion in FY 2017, which would fully offset the amounts proposed for DHS and would offset half of the amounts proposed for DOD.” In laymen’s terms, lots of things are getting cut, the military is getting more money and the budget is expanding by a minor amount.[i],[ii]

THE FRENCH ARE ABOUT TO MAKE WAVES

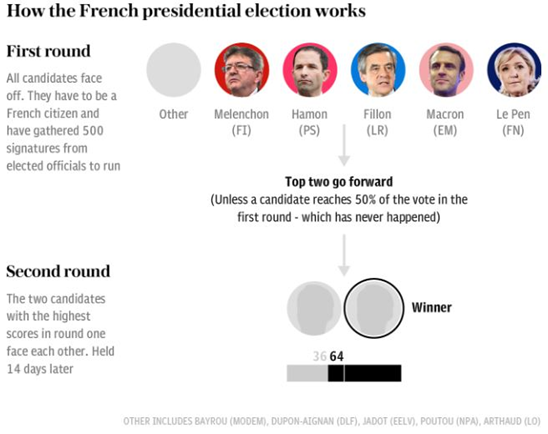

We wrote in January, aside from the inauguration of President Trump, the big event on the calendar in the first half of 2017 is the French Presidential Election. On April 23rd French voters will head to the polls narrowing down the current list of candidates to two. Then on May 7th, barring a historic vote in April, the final vote will take place. The graphic below lists the major candidates as well as the process. The expected result is for the long time front runners, Emmanuel Macron and Marine Le Pen, to face off in the finale. Macron is a centrist-outsider candidate having never been elected to political office. Le Pen is the Trump style candidate and the name of her party speaks for itself, National Front.[iii],[iv]

A third candidate has surged in the polls as of late making the election even more exciting. Jean Luc Melanchon is possibly farther left than Le Pen is right. We do not purport to be experts in French politics, however, with the current polling there is potential for a far-left versus far-right run-off where both candidates are in favor of a French exit of the EU. Ultimately, the survival of the European Union, or the lack there-of, is what has us most interested in the election. A Eurosceptic President of the 2nd largest economy in a faltering European Union has far reaching consequences.[v]

The impact on the price of sourdough and wine is not the issue. The potential for further erosion of stability in one of the major economic blocs in the world is our highest concern. Destabilization of the Eurozone was a topic last year with ‘The Brexit’, and the French election puts the European Union front and center once again. The following is a what-if: a weakening Eurozone will cause a strengthening in the dollar making it harder for US exports to be attractive overseas. A boon for US tourists will be a bane for US exporters. As jobs are impacted there will be a lag effect in the US likely leading to economic weakness for some period of time. Repricing various national currencies, labor markets and export/import markets, and trade agreements will take time and cause drag on the markets. The question is about the depth of the global recession rather than the likelihood of a global recession.[vi]

It is important to note that French bonds are currently trading at double the normal volume as we move closer to the election. Markets are not sure what is going to happen and that has a lot to do with the unexpected outcomes of the British vote to leave the EU and the US vote to elect President Trump.[vii]

WHY THE EU CONTINUES TO MATTER

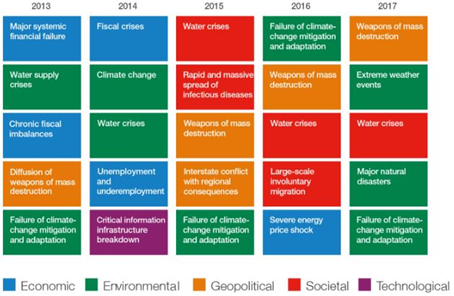

The Maastricht Treaty, signed on February 7th 1992, integrated the European Union and codified the four freedoms central to the EU agreement: freedom of movement in people, goods, money and services. In 2016 the free movement of people was obliquely listed as a potential danger to the global economy in reference to “Large Scale Involuntary Migration” by the World Economic Forum. The graph below should be read from the top down with items on top having more potential to be economically damaging as the issue below.[viii]

Source: World Economic Forum, The Matrix of Top 5 Risks from 2007 to 2017

There are 28 EU Member states under the adopted framework of a single market with free movement of goods, services, people and money. $16.27 trillion in combined GDP is represented by the member nations with a gross population estimated to be around 515 million. What used to be a set of trade agreements country-by-country is now summed in a single block of import/export dollars between the US and the EU covering around $1.1 trillion in goods and services between the two partners. The EU countries as a whole are the 2nd largest export market for the United States. If nothing else, these figures should serve as confirmation that we are a globally connected economy and that what is happening in Europe has the possibility of hitting very close to home.[ix]

The risk is that an irrelevant European Union or an imploded European Union will make a global response to the risks listed above more challenging. Coordinated global responses are already complicated. Taking 28 EU member states and making them, once again, autonomous political and economic units will make any global consensus, cooperation and growth more challenging.[x]

AN AGED BULL MARKET EXPANSION

For investors this is a curious time. The length of the current bull market is not quite in uncharted territory, but it is getting close. This is now the 2nd longest bull market run in history at 98 months and is the second largest on record in terms of percentage growth at 249%. Interestingly, it is a laggard in terms of true economic growth with GDP measurements running at 75% of historic averages, 2.1% versus 2.8%.[xi]

It is in this context that President Trump’s focus on growth and inflation find an audience. The Federal Reserve is leaving open wiggle room for them to step back from the interest rate increases they have initiated in prior meetings. In the most recent Federal Reserve minutes from the March 15th, 2017 meeting the Fed Governors state that, “the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data”. Roughly translated as, we aren’t really sure where economic growth is going right now. Just in case it does not go in a positive direction, we want you to know we will continue our accommodative monetary policy.[xii]

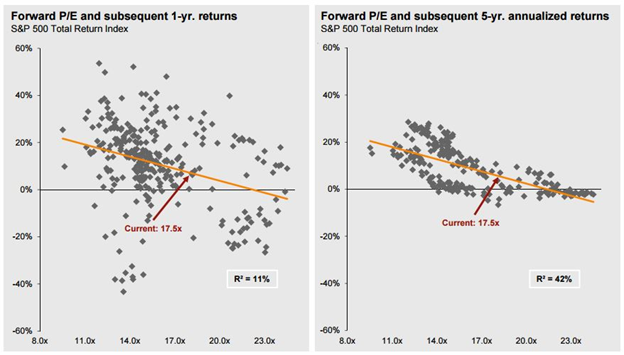

Markets are not cheap by any measure. Price-to-Earnings (PE) multiples are above long-term averages, the Cyclically Adjusted Price-to Earnings (CAPE) is above its long-term average, the Dow and S&P are at absolute high-water marks. As prices creep up and uncertainty of any kind is triggered the natural response is worry.

Source: Factset, Reuters, Standard & Poor’s, J.P. Morgan Asset Management, Guide to the Markets, US, 2Q, as of March 31, 2017

As evidenced above, markets have a tendency to trend down over 1 and 5-yr periods as stock prices get more and more expensive as measured by Price-to-Earnings (PE) multiples. In our opinion, a reasonable conclusion based on the data is for future returns to be more muted going forward than they have been in the past 8 years. This does not mean we recommend avoiding stocks; it does serve to reinforce the importance of having a defined investment philosophy grounded in sound principles, invested well and revisited on a consistent basis.

INVEST SMARTER

Professor Harry Markowitz is a Nobel prize winning economist famous for developing the basis of modern investing philosophy called Modern Portfolio Theory. We have talked about MPT in past quarterly updates so we won’t spend much time on it here. The gist of it is that for any given risk tolerance there is a basket of securities which will reduce portfolio risk and create long term return. Prof. Markowitz is an oft-quoted titan of finance with a gift for cutting through nonsense with common sense – “To reduce risk it is necessary to avoid a portfolio whose securities are all highly correlated with each other.”[xiii]

As returns get harder to come by in the near to mid-term this quote matters a lot.

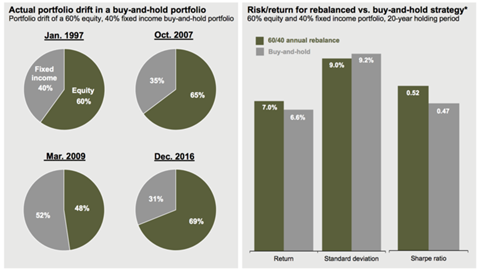

First and Foremost – Rebalancing and Risk Management

Source: Standard & Poor’s, Barclays, FactSet, J.P. Morgan Asset Management, Guide to the Markets, US, 2Q, as of March 31, 2017. Annual Rebalance and Buy-and-Hold strategies are composed of S&P 500 and Barclays U.S. Aggregate total return indexes on a monthly basis

Prudent investing requires managing your portfolio to both an asset allocation strategy and a risk tolerance. The graphs above represent a hypothetical moderate allocation portfolio with a start date of January 1997. Over the course of 20 years this hypothetical portfolio with a 60/40 split and a buy-and-hold strategy evolved into a more growth oriented portfolio with a 69/31 tilt. Total return over time was reduced, standard deviation increased and the measurement of the average return over time was less. The conclusion, not maintaining your risk tolerance via rebalancing over time can lead to more risk and less return than anticipated.

Second – Reduce Bad Behaviors like Bias

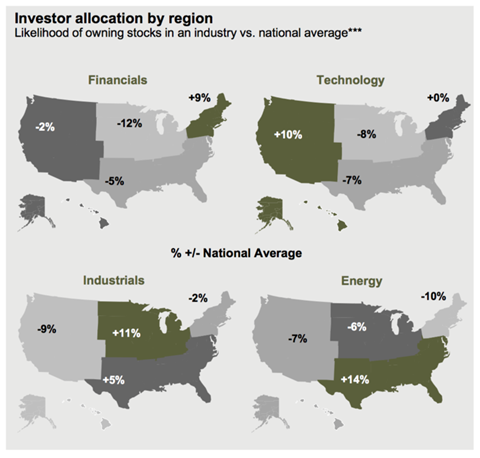

Do we invest in what we invest in because we should? Or because those around us invest similarly regardless of appropriateness, risk, quality, need? If we look at investment patterns across the United States some interesting data points are brought to light.

Source: Openfolio, IMF, ICI, J.P. Morgan Asset Management, Guide to the Markets, US, 2Q, as of March 31, 2017

***Investor allocation by region is based on data collected by Openfolio. Average sector allocations at the national level are determined by looking at the sector allocations of over 20,000 brokerage accounts, and taking a simple average. Portfolio allocations are then evaluated on a regional basis, and the regional averages are compared to the national average to highlight any investor biases. Further details can be found on openfolio.com

Those living in the financial center of the US, the New York and New England area, are more likely to invest in financials. Those living on the West Coast where tech titans such as Microsoft, Apple and Facebook are centered, tend to invest in technology. Investors in the upper Midwest are more likely to invest in Industrials such as auto manufacturers and the related suppliers. Those in the south where most of our energy industry is located for refinery’s and energy transport are more likely to invest in the energy sector.

Likewise, US Investors are much more likely to allocate a disproportionate share of their investable assets in the US relative to Global equities. The US represents 36% of global stock and bond markets yet US investors will invest on average 74% of their portfolio in domestic stock. The best performers year-to-date are international stocks. Being overinvested in US stocks might have been a winning strategy in prior years, but to date 2017 is shaping up a bit different.[xiv]

It is easy to fall prey to investing in what we know based on where we live and who we talk to. Echo chambers are powerful. Behavioral biases are hard to overcome. Modern Portfolio Theory is more important today than ever when we are approaching what appears on the surface to be a politically frought time period with expected low market returns. Diversification involves letting go of bias and striving to own as much of the market as is allowable for your individual risk tolerance.

LOOKING FORWARD

The Federal Reserve summed up our current economic and market circumstances well in their last meeting:

“Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.”

There are known issues looming, such as the French Presidential Election and the developing nuclear staredown with North Korea. There are unknown issues always possible such as a major natural disaster or terror event. Sound investing does not prevent these things from happening. But it can go a long way towards preventing global events from impacting your long term goals. We are here to help you make rational, informed and well-reasoned decisions in spite of the challenges ahead.

We thank you for your continued trust and support. Your input is always welcome and we ask that you contact us with any questions or concerns.

DISCLOSURE

All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards.

Investing in securities in emerging markets involves special risks due to specific factors such as increased volatility, currency fluctuations and differences in auditing and other financial standards. Securities in emerging markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments.

An index is a statistical measure of change in an economy or a securities market. In the case of financial markets, an index is an imaginary portfolio of securities representing a particular market or a portion of it. Each index has its own calculation methodology and is usually expressed in terms of a change from a base value. Thus, the percentage change is more important than the actual numeric value. An investment cannot be made directly into an index.

Investing in fixed income securities involves credit and interest rate risk. When interest rates rise, bond prices generally fall. Investing in commodities may involve greater volatility and is not suitable for all investors. Investing in a non-diversified fund that concentrates holdings into fewer securities or industries involves greater risk than investing in a more diversified fund. The equity securities of small companies may not be traded as often as equity securities of large companies so they may be difficult or impossible to sell. Neither diversification nor asset allocation assure a profit or protect against a loss in declining markets. Past performance is not an indicator of future results.

Securities offered through 1st Global Capital Corp., Member FINRA and SIPC. Bruce Rawdin-Baron, Steven W. Pollock, Sean P. Storck, Matthew J. Anderson and Nicole Albrecht are Registered Representatives of 1st Global Capital Corp. Investment advisory services, including RBFI portfolios offered through Reason Financial. IMS platform accounts offered through 1st Global Advisors, Inc. Reason Financial. and 1st Global Capital Corp. are unaffiliated entities. Reason Financial is a Registered Investment Adviser. Placing business through 1st Global Insurance Services. Registration does not imply a certain level of skill or training. We currently have individuals licensed to offer securities in the states of Arizona, California, Illinois, Indiana, Kansas, Massachusetts, Michigan, New York, Oregon and Washington. This is not an offer to sell securities in any other state or jurisdiction. CA Department of Insurance License: Bruce Rawdin-Baron #0736631, Steven W. Pollock #OE98073, Sean P. Storck #0F25995, Matthew J. Anderson #0F21959 and Nicole Albrecht #0F99962.

Copyright © 2017 Reason Financial all rights reserved.

Reason Financial

4747 Morena Blvd, Suite 102, San Diego, CA 92117

ENDNOTES

[i] President Trump. Presidential Memoranda, “Text of a Letter from the President to the Speaker of the House of Representatives”. The White House. 16 March 2017.

[ii] Harrington, Rebecca. “Trump Has Already Signed 64 Executive Actions – Here’s What Each One Does”. Business Insider.com. Business Insider. 12 Apr 2017. Web. 15 Apr 2017.

[iii] Samuel, Henry. “How Does the French Political System Work and What Are the Main Parties?”. http://www.telegraph.co.uk/news/0/does-french-political-system-work-main-parties/. The Telegraph. 6 Apr 2017. Web. 12 Apr 2017.

[iv] Beardsley, Eleanor. “Political Outsider Emmanuel Macron Campaigns To ‘Make France Daring Again’”. http://www.npr.org/sections/parallels/2017/02/28/517498543/political-outsider-emmanuel-macron-campaigns-to-make-france-daring-again. NPR (National Public Radio). 28 Feb 2017. Web. 15 Apr 2017.

[v] Wikipedia, The Free Encyclopedia. Wikipedia, The Free Encyclopedia, 17 Apr 2017. Web. 17 Apr 2017.

[vi] Garret, Oliver. “An Investor’s Guide to the Collapse of the European Union.” https://www.forbes.com/sites/oliviergarret/2017/03/01/an-investors-guide-to-the-collapse-of-the-european-union/#16dc94cff805. Forbes.com. 1 Mar 2017. Web. 09 Apr 2017.

[vi] Moore, Elaine and McCrum, Dan and Fortado, Lindsay. “French Bond Trading Soars On Fear Of Populist Wave.” https://www.ft.com/content/0f1fdff6-f469-11e6-95ee-f14e55513608. Financial Times. 16 Feb 2017. Web. 17 Apr 2017.

[viii] World Economic Forum. “Top 5 Global Risks in Terms of Likelihood”. http://reports.weforum.org/global-risks-2017/the-matrix-of-top-5-risks-from-2007-to-2017/. World Economic Forum. Web. 15 Apr 2017.

[ix] Central Intelligence Agency. “The World Factbook”. https://www.cia.gov/library/publications/the-world-factbook/geos/ee.html. Central Intelligence Agency. 17 Apr 2017. Web. 17 Apr 2017.

[x] Office of the United States Trade Representative. “European Union”. https://ustr.gov/countries-regions/europe-middle-east/europe/european-union. Office of the United States Trade Representative. 17 Apr 2017. Web. 17 Apr 2017.

[xi] J.P. Morgan Asset Management. “Guide to the Markets, US, 2Q, as of March 31, 2017.”

[xii] Federal Reserve Press Release March 15, 2017. https://www.federalreserve.gov/monetarypolicy/files/monetary20170315a1.pdf. Federal Reserve Board of Governors. 15 Mar 2017. Web. 17 Apr 2017.

[xiii] Gaille, Brandon. “15 Fascinating Harry Markowitz Quotes.” http://brandongaille.com/15-fascinating-harry-markowitz-quotes/. 17 Nov 2016. Web. 17 Apr 2017.

[xiv] J.P. Morgan Asset Management. “Guide to the Markets, US, 2Q, as of March 31, 2017.”